Iran Conflict vs. the AI Capex Cycle

We wanted to address recent market volatility tied to the conflict with Iran and the potential for continued disruption in the Strait of Hormuz. Comparisons to past energy crises—most notably 1973—are understandable, but we believe the current backdrop is more nuanced.

At the core, markets are balancing two powerful forces:

- A strong structural earnings backdrop driven by AI investment

- A traditional macro shock tied to energy and geopolitics.

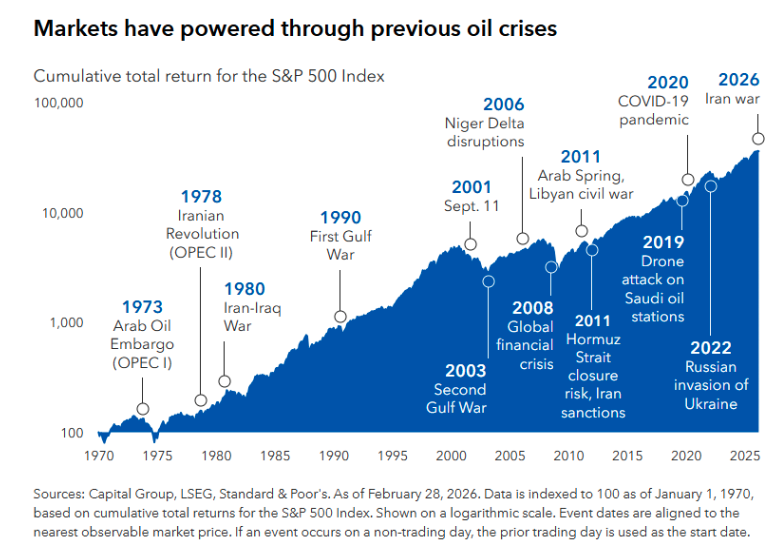

Our view, for long-term investors this is not a moment to exit markets. While risks are real, underlying support remains intact. Historically, many investors have benefited from maintaining discipline around long-term investment plans rather than attempting to time market movements. (See below chart for market reactions to previous oil crises).

*Past performance is not indicative of future results. Index performance is shown for illustrative purposes only. Investors cannot invest directly in an index. Historical market responses to geopolitical events may differ substantially from future market behavior.

Below, we outline both sides (Bear and Bull Cases) of the equation and how we believe investors should think about positioning.

The Bear Case: Understanding the Risks

1) The Strait of Hormuz is a system-level risk, not just a headline

Approximately 20–25% of global oil flows through this passage. A prolonged disruption could remove a meaningful share of supply—potentially exceeding the scale of the 1973 shock.

2) Energy shocks can ripple through the entire economy

The transmission mechanism is familiar: higher energy prices feed inflation, which can delay or reverse central bank easing and pressure equity valuations.

3) Profit margins are the hidden vulnerability

Corporate margins remain near historical highs (roughly 13–16%). Higher energy costs alongside ongoing wage pressures could compress margins, creating risk not through falling revenues, but through earnings disappointments versus elevated expectations.

4) The AI investment cycle carries its own risks

The scale of AI-related capital spending is historically large, with some companies investing beyond current free cash flow and relying on capital markets. This model depends on sustained demand and stable financing conditions—both of which could be tested if macro conditions tighten.

5) Comparisons to 1973: useful, but imperfect

There are similarities, namely an oil shock that can drive inflation and recession fears. However, there are also key differences:

- The United States is now a major energy producer

- Oil represents a smaller share of total energy usage today

- The U.S. economy is significantly more services and technology-oriented TODAY.

Additionally, the 1973 market downturn occurred alongside pre-existing economic fragility (high inflation, policy missteps, and structural shifts in the monetary system). That exact combination is not present today.

The Bull Case: Why the Foundation Remains Strong

1) Earnings growth is robust and driving the market

Corporate earnings remain robust, with growth well above long-term averages. Importantly, market returns are being supported primarily by profit growth rather than multiple expansion. A majority of companies continue to exceed expectations, providing a fundamental cushion.

2) The AI investment cycle is real and significant

Many large technology companies are currently committing significant capital toward AI-related infrastructure, representing one of the most significant multi-year investment cycles in recent history. The spending is visible, ongoing, and something we believe could likely extend over several years.

3) Valuations have moderated somewhat

While valuations remain above long-term averages, they have moderated from earlier in the year. Current levels reflect strong earnings growth, high margins, and continued investment-led expansion, making the market less stretched and more fundamentally supported.

4) Markets are forward-looking and already adjusting

Markets have shown resilience despite geopolitical escalation. Historically, equities tend to stabilize before macro uncertainty is resolved. If any energy disruption proves temporary, a meaningful portion of the risk may already be reflected in prices.

Balancing the Two: What the Market is Pricing (and our Base Case)

Markets today appear to be pricing a contained energy shock alongside continued earnings strength. The following represents our current assessment:

- Energy disruption is temporary or partially constrained

- Oil prices remain elevated but do not spike sustainably

- Economic growth slows modestly but remains positive

- AI-driven investment continues largely uninterrupted

Under this scenario, earnings growth continues to support markets, even if volatility remains elevated.

This outlook depends on:

- Oil price increases being contained in duration and magnitude

- Inflation remaining manageable

- Financial conditions staying supportive of continued investment.

The outlook would be challenged if:

- Energy disruption becomes prolonged

- Inflation re-accelerates materially

- Interest rates rise further, pressuring both valuations and capital spending.

Should Investors Move to Cash?

We do not believe this environment calls for a wholesale shift to cash.

1) Market timing is rarely successful

Markets are not binary, and geopolitical outcomes are inherently uncertain. Exiting and re-entering at the right moments is extremely difficult, and missed rebounds can be costly.

2) The market is balancing risk, not ignoring it

Current volatility reflects a market weighing strong earnings against macro uncertainty, not one in freefall.

3) Markets recover before clarity emerges

Historically, markets have often recovered ahead of macro certainty, meaning waiting for clarity often results in re-entry at higher levels.

4) Focus on positioning, not panic

Rather than exiting the market entirely, it is more productive to evaluate portfolio exposures:

- Are you overly concentrated in certain high-growth areas?

- Do you have exposure to sectors that benefit from higher energy prices?

- Are your holdings characterized by strong balance sheets and pricing power?

Conclusion

The AI-driven investment cycle remains a powerful and durable support for earnings and markets. At the same time, potential disruption in the Strait of Hormuz represents the key macro risk.

While this does not currently resemble 1973, it could evolve into a more meaningful headwind if energy constraints persist. Duration, not just magnitude, will be critical.

In our view, this is not a “move to cash” moment, but a period where macro risks may temporarily overshadow otherwise strong fundamentals.

As always, we remain focused on navigating both opportunity and risk with discipline and perspective.

Sources: FactSet, Capital Group, LSEG, Standard & Poor

This material is for informational and educational purposes only and should not be construed as investment advice or a recommendation to buy or sell any security. The views expressed represent current opinions as of the date of publication and are subject to change without notice. Forward-looking statements are based on current expectations and assumptions and are subject to risks and uncertainties. Actual results may differ materially. Investors should consult with their financial professional regarding their specific circumstances before making investment decisions.

Acumen Wealth Advisors®, LLC is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where Acumen Wealth Advisors®, LLC and its representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by Acumen Wealth Advisors®, LLC unless a client service agreement is in place.